From the ivy-covered cloisters of Harvard, Yale, and Princeton to the T-shirt- clad students of your local junior college, wherever the subject of economics is studied and discussed, one name is preeminent: John Maynard Keynes. A sacred hush falls over the classroom when his name is spoken. All jokes must cease about economists with wire-rimmed glasses holing up in their cubicles trying to see if what they just observed in real life can be massaged around to fit their pet economic theory. It is expected that if a professor or student utters his name they must do so in soft, reverent tones, and then place their fingers to their pursed lips and gently touch the printed name on the page of their classical textbook. Just who is this John Maynard Keynes?

The sacred legend holds that in the hours of deepest distress, when the United States was not just reeling from the bludgeoning blows of the Great Depression, but was down and out for the final count, never to arise again from the smoldering ashes of dissipated wealth and shattered culture, John Maynard Keynes came riding to the rescue. It was Keynesian economic philosophy, emanating like a bright beacon light from the halls of King’s College in Cambridge, England, that saved the culture and probably the universe.

As the legend goes, John Maynard Keynes assembled his exclusive teachings into a printed book, The General Theory of Employment, Interest, and Money, that was printed in 1936. Miraculously, the newly elected president of the United States, Franklin D. Roosevelt, stumbled across the book just in time, read the magic words, arduously and meticulously implemented the teachings, and the floundering nation was transformed into the economic super-power that held sway over the entire world like no other nation in history. How could anyone with half a brain and one eye ever dispute or even question those sacred writings that were passed down to this favored nation so many years ago? Blessed is the name of John Maynard Keynes.

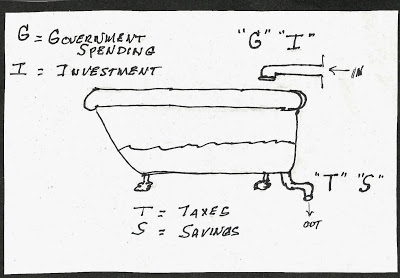

So, just what were those original teachings? My major professor in economics, Dr. Paul Ballantyne of the University of Colorado, one day told me, “Jim, if you want to easily remember the economic philosophy of Professor Keynes, just visualize in your mind a bathtub. It is about one-third full of water. Above the bath tub is a spigot with a handle to regulate the inflow of water. Above the spigot are the letters “G” and “I.” Those letters stand for Government and Investment.

As with all bathtubs, there is a drain at the bottom of the tub. Over the drain are the letters “T” and “S.” They stand for Taxes and Savings.

If you want to fill up and regulate the economy you turn on the “G” and “I” spigot and plug the “T” and “S” drain pipe. By increasing the Government Spending and Investment faster than the leakage of Taxes and Savings out of the economy, you can increase the level of income and reduce unemployment.

“But,” I protested to Dr. Ballantyne, “what’s so brilliant and new about that? Explicit provisions were made for that clear back in 1913 when the U.S. passed the Federal Reserve Act. The Federal Reserve was given certain rights:

- The Feds were given the right to raise or lower the percentage of reserves that the banks must keep on hand. If they lowered the amount of required reserves, then the banks would have more money to lend out to customers to invest in their projects. The higher the reserves imposed on the banks, the less money could go into the system.

- The Feds have the right to raise or lower the Discount Rate of the money they can lend to the banks to lend to their customers. The higher the discount interest rate, the less the banks will borrow from the Feds, and the less will be available to the customers, and the less money will be introduced into the system. The lower the discount rate, the more likely the banks will borrow from them and lend the money out to their customers, and more money will find its way into the system, and there will be an increase in employment.

- The Feds have the right to sell and buy back notes and securities to citizens and foreigners to cover the debts the government creates because of their desire to spend more than they have in their account.

How much more could they want? What’s new about Keynes?”

John Maynard Keynes had the advantage of watching Great Britain go through an earlier depression of its own. He was in England and only twenty-nine years old when the U.S. passed the Federal Reserve Act. He was also able to watch what had happened during the recessions of the U.S. and the early years (1929 – 1935) of the Great Depression before he wrote his book. He was convinced that the severe bumps of the boom and bust economic cycles could be flattened out with his aggregate expenditures model. He declared that Say’s Law was not dependable, and if the economy were left to correct itself it would not happen. He pointed to the Great Depression as his needed proof.

But why the God-like treatment for Keynesian economics? All of the tinkering with aggregate expenditures did not lift the U.S. out of the Great Depression. Successful economies are built on production. They have to produce something, and it was not until the U.S. began production for the buildup for World War II that employment and incomes began to rise. Indeed, World War II was a horrible price to pay to end the Great Depression.

John Maynard Keynes did not leave any question as to government’s economic involvement. He felt it was the government’s responsibility to be in control of the stability of the national economy and play an active role in the policies and procedures. He also was a strong advocate of the government’s control of housing and ownership of utilities and transportation. Recent polls indicate that 70% to 80% of today’s economists subscribe to the ideas associated with the Keynesian approach that business cycles should be managed by the Fed. That comes close to divinity.

Next week we will look at Franklin D. Roosevelt.

(Research ideas from Dr. Jackson's new writing project on Cultural Economics)

© Dr. James W. Jackson

Permission granted by Winston-Crown Publishing House